The Retirement Gap Years

The Gap Years: Understanding Key Retirement Milestones to Maximize After-Tax Wealth

Written by: Harmony Wagner, CFP, CPWA

Many young professionals in their working years focus on building their wealth. As retirement approaches, the impact of taxes narrows the focus to maximizing the after-tax value of one’s wealth. With required minimum distributions on the horizon, a period of time referred to as the “retirement gap years” allows for strategic actions to help spread tax burden as efficiently as possible.

When IRA owners reach RMD age, they are required to pull a certain percentage of their IRAs each year, paying ordinary income tax on those withdrawals. The requirement presents a constraint on taxable income. In addition to RMDs, IRAs face a second implication when it comes to passing to beneficiaries. For most non-spouse beneficiaries (children, grandchildren, siblings, etc), IRAs must be distributed (and taxed) within 10 years of inheritance. These can present some tax situations where IRA dollars are taxed at high rates.

Due to the rules around IRA distributions and taxation, many IRA owners can benefit from pro-active IRA management that typically takes one of three forms:

- Roth Conversions – Converting IRA dollars (and paying taxes now) to a Roth IRA where all future growth and distributions are tax-free for the original owner and/or their beneficiaries

- IRA Withdrawals – Planning IRA withdrawals for cash flow needs prior to when they are required to cover cash flow needs

- Tax-Free Charitable Donations – Making any desired charitable donations from an IRA to move funds out on a tax-free basis

How can a retiree determine which of these strategies to use and when? It’s important to understand the ways that tax situations change throughout retirement based on changing income sources and other factors. Let’s discuss the key milestones in the gap years and how retirees can take advantage of this important window.

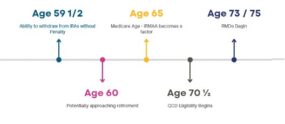

→ Age 59 ½ - At age 59 ½, IRA owners are able to withdraw from their IRAs without

early withdrawal penalties. While it may not make sense to withdraw from the

IRAs right away, it does open some doors to the possibility of utilizing IRA

withdrawals to fill up lower tax brackets whenever possible.

→ Age 60 – You may now be officially retired, or at least thinking about it. Once you

no longer have earned income, your tax picture may allow Roth conversions

and/or making withdrawals from IRAs at low tax rates.

→ Age 62 – you are potentially eligible to collect Social Security; however, it might

not make sense to collect benefits immediately. By holding off Social Security,

you can allow your benefits to increase, and also keep your taxable income low,

allowing for more IRA withdrawals in the early years.

→ Age 63 – Eligibility for Medicare doesn’t begin until age 65, but there is a 2-year

lookback period for IRMAA Medicare premium increases, meaning retirees must

start planning for income-related premium adjustments 2 years prior to eligibility.

This can be a limiting factor on taxable income as any additional income may

cause you to pay more in premiums in the future.

→ At age 70 ½ - IRA owners are allowed to make tax-free charitable donations

directly from their IRAs, reducing the IRA balance without paying taxes.

→ Age 73 or 75 – Depending on your birth year, you’ll be required to start RMDs at

either 73 or 75. At that point, any Roth conversions must happen after the RMDs

have been satisfied.

As retirees move through these important milestones, there may be “gap” years

where Roth conversions are more appealing due to the changing tax landscape as

Social Security, Medicare, and other elements come into play. By analyzing the tax

situation of each year individually, retirees can determine the best approach for

conversions, withdrawals, and charitable donations to strategically improve their after-

tax wealth.

Contact our office if you’d like to hear more about how a pro-active IRA

management approach can benefit you.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Bouchey Financial Group, Ltd. [“Bouchey Financial”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, no portion of this discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Bouchey Financial. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Neither Bouchey Financial’s investment adviser registration status, nor any amount of prior experience or success, should be construed that a certain level of results or satisfaction will be achieved if Bouchey Financial is engaged, or continues to be engaged, to provide investment advisory services. Bouchey Financial is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Bouchey Financial’s current written disclosure Brochure and Form CRS discussing our advisory services and fees is available for review upon request or at www.bouchey.com. Please Note: Bouchey Financial does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Bouchey Financial’s web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a Bouchey Financial client, please contact Bouchey Financial, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.