Investing 101: Understanding the Different Types of Accounts

Written by: Scott Strohecker, EA

Investing is a critical component of building wealth and securing your financial future. However, before you can start investing, it is important to understand the different types of accounts available to you. From retirement accounts to taxable brokerage accounts, each type of account has its own rules, tax implications, and investment options. This blog will explore the various types of investment accounts and how they can help you reach your financial goals.

Retirement Accounts: Retirement accounts are designed to help individuals save for retirement while offering tax advantages to encourage long-term savings. Common types of retirement accounts include:

- 401(k): Employer-sponsored retirement plans that allow employees to contribute a portion of their pre-tax income to a retirement account. Some employers may offer matching contributions, effectively doubling the amount you save. Some employer plans now offer a Roth 401(k), in which you can after-tax contributions.

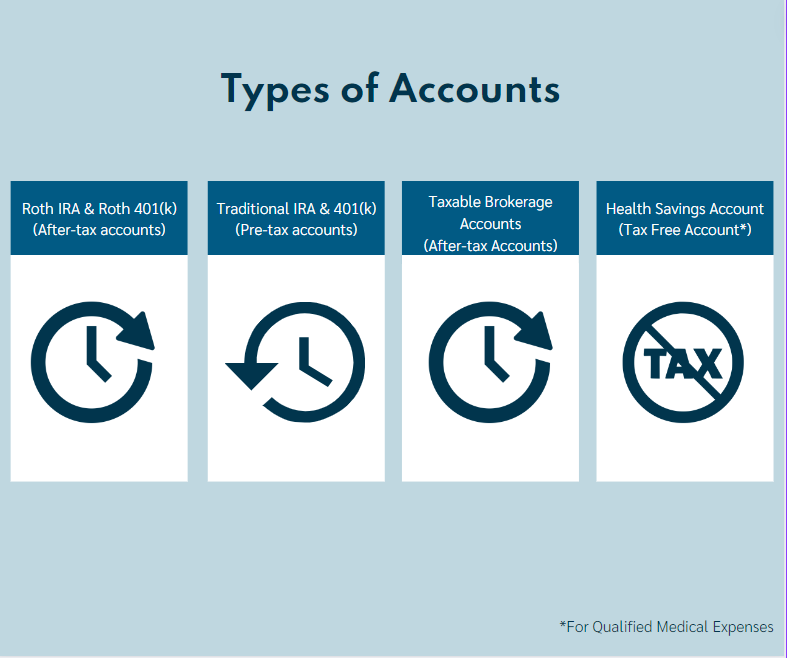

- Individual Retirement Accounts (IRAs): IRAs are retirement accounts that individuals can open on their own. There are two main types of IRAs: traditional IRAs, which offer tax-deferred growth, and Roth IRAs, which provide tax-free withdrawals in retirement.

Taxable Brokerage Accounts: Taxable brokerage accounts are investment accounts that are not subject to the same tax advantages as retirement accounts. While contributions to these accounts are made with after-tax dollars, they offer more flexibility in terms of investment options and withdrawal rules. Investors can buy and sell stocks, bonds, mutual funds, and other securities within these accounts without restrictions on when they can access their funds.

Education Savings Accounts: Education savings accounts, such as 529 plans and Coverdell Education Savings Accounts (ESAs), are designed to help families save for education expenses, including tuition, books, and room and board. Contributions to these accounts grow tax-free, and withdrawals are tax-free when used for qualified education expenses. Thanks to the SECURE ACT 2.0, 529 plans now offer more flexible than ever before.

Health Savings Accounts (HSAs): HSAs are tax-advantaged accounts that individuals can use to save for qualified medical expenses. Contributions to HSAs are tax-deductible, and withdrawals for qualified medical expenses are tax-free. HSAs offer a triple tax advantage, making them a powerful tool for both saving for healthcare costs and supplementing retirement savings.

Employer Stock Purchase Plans: Some employers offer stock purchase plans that allow employees to purchase company stock at a discounted price. These plans often come with favorable tax treatment, such as the ability to purchase stock at a discount and defer taxes on the gains until the stock is sold.

Conclusion: Understanding the different types of investment accounts is crucial for developing a comprehensive financial plan. Whether you're saving for retirement, education, or other financial goals, choosing the right accounts can help you maximize tax advantages and grow your wealth over time. By taking advantage of tax-advantaged accounts and investing wisely, you can build a secure financial future for yourself and your family.

If you have any questions about the different types of accounts and would like to speak with a financial advisor, you can contact our team for more information.

Related Blogs:

6 Strategies for Unused 529 Plan Funds

Health Savings Accounts Can Be an Integral Part of Your Retirement Plan – Here’s How

Bouchey Financial Group has offices in Saratoga Springs and Historic Downtown Troy, NY as well as Boston, MA and Jupiter, FL.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Bouchey Financial Group, Ltd. [“Bouchey Financial”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, no portion of this discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Bouchey Financial. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Neither Bouchey Financial’s investment adviser registration status, nor any amount of prior experience or success, should be construed that a certain level of results or satisfaction will be achieved if Bouchey Financial is engaged, or continues to be engaged, to provide investment advisory services. Bouchey Financial is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Bouchey Financial’s current written disclosure Brochure and Form CRS discussing our advisory services and fees is available for review upon request or at www.bouchey.com. Please Note: Bouchey Financial does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Bouchey Financial’s web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a Bouchey Financial client, please contact Bouchey Financial, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.