Wealth Management Albany NY | Fee-Only Fiduciary

You've spent decades building your wealth. The next chapter is about making it work for you.

If you're approaching retirement with $2 million or more in investable assets, you already know your financial life is about to get more complex, not less. Pension decisions, Social Security timing, tax-efficient drawdown strategies, equity compensation, estate considerations, and the simple but enormous question: can I live the life I want in retirement?

Bouchey Financial Group, headquartered in Troy with offices in Saratoga Springs and Boston, has operated as a 100% fee-only, fiduciary Registered Investment Advisor since 1995. Every recommendation we make is legally and ethically required to serve your best interests, not ours.

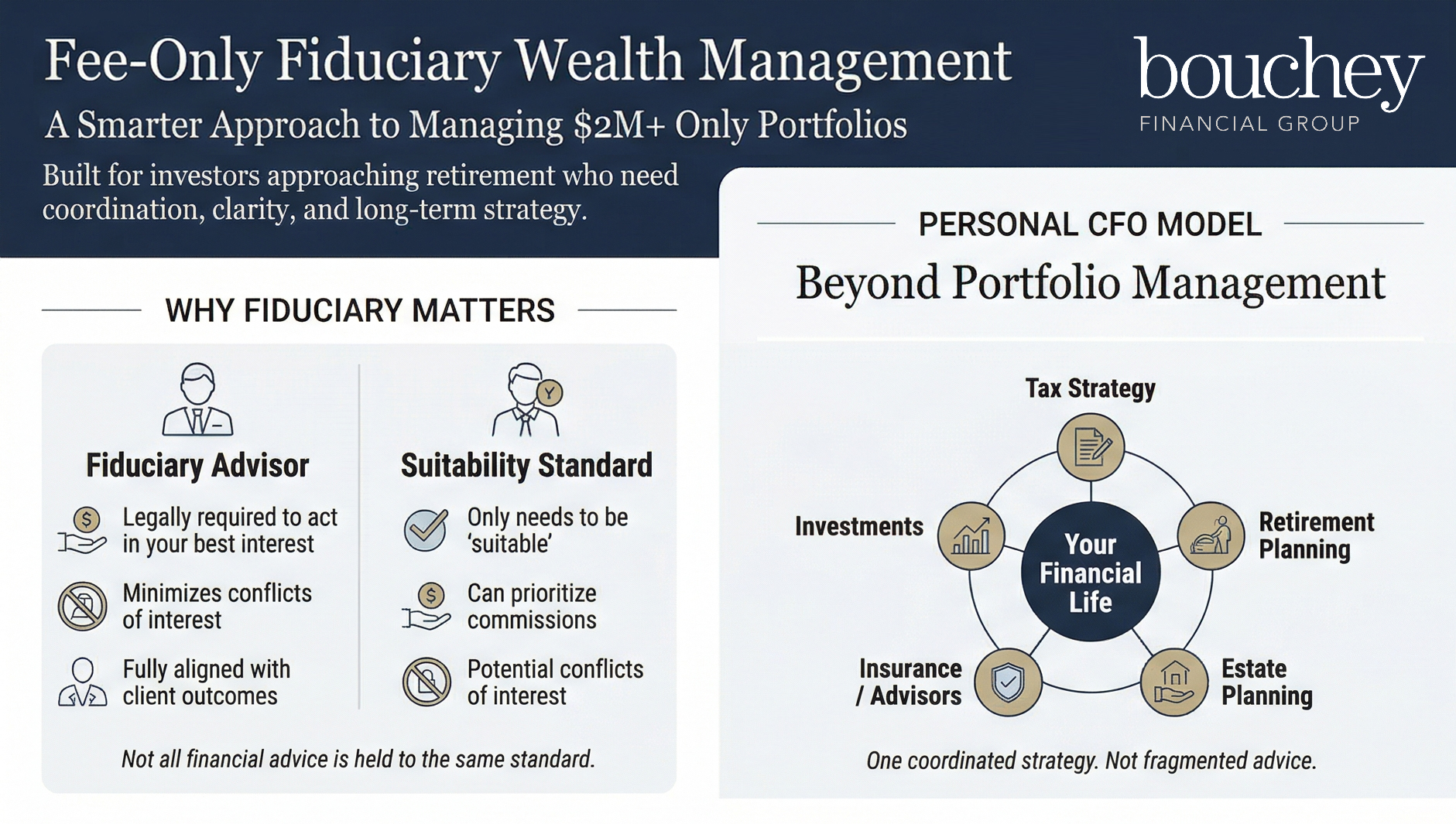

Why "Fiduciary" Isn't Just a Buzzword

A fiduciary is someone legally obligated to act in your best interest at all times. According to the SEC's Standards of Conduct for investment advisers, registered investment advisers must understand a client's full financial profile and place client interests above their own — including minimizing conflicts of interest wherever possible.

This is meaningfully different from the "suitability" standard that applies to broker-dealers, which only requires that a recommendation be suitable — not necessarily optimal — for the client. That distinction has significant real-world consequences for the advice you receive and the products you're sold.

Fee-Only vs. Fee-Based

These two terms are often confused — and sometimes deliberately so. A fee-only advisor is compensated solely by the client, through a flat fee, hourly rate, or percentage of assets under management. A fee-based advisor, by contrast, can also earn commissions from third parties on products they recommend.

| Compensation Model | Client Pays | Advisor Also Earns Commissions? |

| Fee-Only | Yes | No |

| Fee-Based | Yes | Yes — from product salesAdvisor Also Earns Commissions? |

| Commission-Only | No direct fee | Yes — from product sales |

Steven Bouchey adopted this model in the early 1990s, well before fee-only became an industry trend. It wasn't the easy path — most advisors at the time earned their living on commissions. But it was the right one, and it's been the foundation of every client relationship since.

Your Personal CFO — Not Just a Portfolio Manager

Most wealth managers manage investments. We manage your entire financial life.

The Personal CFO model means Bouchey Financial Group serves as your financial command center; the single point of coordination between your investments, your tax strategy, your retirement plan, your estate documents, and any outside professionals like attorneys or insurance specialists. You delegate the complexity. We manage it as one integrated team.

Here's what that looks like day to day:

A Team That Knows You

You won't be handed off to a call center or a rotating cast of junior advisors. Each client works with a dedicated team of professionals — a wealth advisor, a financial planner, and a tax specialist — who collaborate on every aspect of your plan. With an advisor-to-client ratio of approximately 1:100, our team has the capacity to know your situation deeply, not just review it once a year.

Proactive Communication, Not Reactive

We don't wait for you to call us. Our advisors initiate semi-annual portfolio reviews to ensure your plan is on track. Between meetings, you'll receive email notifications for every portfolio transaction — each one accompanied by a clear explanation of why the trade was made. No surprises. No black boxes.

A Thorough Onboarding

When you become a client, we don't rush to move accounts and start trading. Our onboarding process takes approximately six months — enough time to conduct a full financial assessment, understand your complete picture, and implement your portfolio and plan thoughtfully. We'd rather get it right than get it fast.

How We Invest: Evidence Over Emotion

Our investment philosophy is built on a straightforward premise: risk-adjusted returns over the long term, driven by discipline rather than market timing or speculation.

Strategic Asset Allocation: We construct portfolios with broad diversification across global asset classes — each selected for its distinct performance characteristics and risk profile. This isn't a set-it-and-forget-it approach; we tactically rebalance by shifting allocations toward undervalued opportunities and trimming overexposure when asset classes become stretched.

Three Strategy Tiers: Depending on your needs and circumstances, our portfolio construction draws from three strategy types: long-term purchases (our primary approach), short-term positions held under one year, and tactical trading within a 30-day window. The blend is tailored to your risk tolerance, time horizon, and tax situation.

Low-Cost, Tax-Efficient Implementation: Index funds make up the majority of our holdings, keeping expense ratios low. Our institutional relationship with Charles Schwab gives clients access to a trading platform where many transactions carry no client-facing transaction costs — a meaningful advantage compounded over decades.

Direct Indexing for Taxable Accounts: For clients with significant taxable assets, we offer direct indexing — owning individual stocks that replicate an index rather than buying a fund. This creates opportunities for granular tax-loss harvesting (selling individual positions at a loss to offset gains elsewhere) and portfolio customization, such as excluding specific sectors or companies. It's one of the fastest-growing strategies in wealth management, and our team has built deep expertise in executing it effectively.

Transparency You Can Verify: Every trade in your account triggers an email notification with a written explanation of the rationale. You'll always know what we did and why. That level of transparency isn't standard in the industry — but we think it should be.

35 Years. One Principle.

Steven Bouchey began advising clients in 1990 with a conviction that was uncommon at the time: clients should always come first. He officially formed Bouchey Financial Group as a registered investment advisor in 1995, building the firm from a solo practice into one of the Capital Region's most established independent wealth management firms.

That growth has been deliberate. Today, firm ownership is shared among the following shareholders:

- Steven B. Bouchey, CFP® — Founder & CEO | Chief Visionary Officer. Host of Let’s Talk Money on WGY.

- Ryan Bouchey, CPA, CFP® — Chief Strategic Officer | Shareholder.

https://bouchey.com/about-us/meet-our-team/ - John Millet, CPA — Chief Operating Officer | Chief Financial Officer | Shareholder.

- Martin X. Shields, CFP®, AIF® — Chief Wealth Advisor | Shareholder.

- Lauren A. Bouchey — Client Concierge | Philanthropy Advisor | Shareholder.

The leadership team is supported by professionals including David W. Clarke (Director of Operations | Chief Compliance Officer), Paolo LaPietra, CFP® (Director of Portfolio Strategy | Wealth Advisor), and Harmony D. Wagner, CFP®, CPWA® (Director of Financial Planning | Wealth Advisor).

With a multi-owner, multi-generational leadership structure already in place, we believe that a succession plan is a core pillar to establishing relationships for decades.

Your Next Step Doesn't Have to Be Complicated

If you're evaluating whether your current financial advisor is acting as a true fiduciary — or whether your tax strategy, investment plan, and retirement drawdown are actually working together — Bouchey Financial Group's Personal CFO model is built to answer exactly that question.

The team's combination of 9 CFP® professionals, 3 CPAs, and in-house tax preparation means your financial plan is coordinated under one roof, not scattered across several firms.

Learn how the onboarding process works →

Frequently Asked Questions

What is the difference between a fiduciary and a non-fiduciary financial advisor?

A fiduciary is legally required to act in your best interest at all times, while a non-fiduciary (such as a broker-dealer operating under the suitability standard) only needs to recommend products that are suitable — not necessarily optimal. The practical difference is that a fiduciary cannot prioritize their own compensation or interests over yours when making recommendations.

Is fee-only the same as fee-based?

No — these terms describe different compensation structures. A fee-only advisor is paid exclusively by the client and earns no commissions. A fee-based advisor can charge client fees and also earn commissions from third parties on the products they sell, which creates potential conflicts of interest that a fee-only model avoids entirely.

Does Bouchey Financial Group only serve clients in the Albany area?

No. While the firm has roots in the Capital Region with offices in Troy and Saratoga Springs, Bouchey Financial Group manages assets for clients in 34 states and overseas. The firm also has offices in Boston, MA, and Saratoga Springs, FL.

What is an ERISA 3(38) Investment Manager, and why does it matter for my company's retirement plan?

An ERISA 3(38) Investment Manager is a firm that assumes full fiduciary responsibility and liability for managing the investments in an employer-sponsored retirement plan. This relieves plan sponsors of the personal liability that comes with selecting and monitoring plan investments — a significant protection for business owners and plan trustees.

How does asset allocation differ from simply diversifying into different mutual funds?

Strategic asset allocation targets specific weightings across global asset classes based on your risk tolerance and goals. Holding several mutual funds doesn't guarantee true diversification if they're concentrated in the same sectors — a structured approach is designed to reduce that correlation risk.

What credentials should I look for when evaluating a wealth management firm?

At minimum, look for the CFP® designation, which requires rigorous exams, experience, and a fiduciary code of ethics. Credentials like CPA, CPWA®, and AIF® signal additional depth in tax planning, private wealth, and fiduciary accountability.

How often should I expect to meet with my wealth advisor?

Best practice for most clients is at least annually for a full financial plan and portfolio review, with additional check-ins as life events occur — such as a job change, inheritance, retirement, or major purchase. At Bouchey Financial Group, advisors proactively reach out to clients for reviews and are accessible by phone and email between scheduled meetings.