Emergency Funds: Why You Need One & How to Build It

Written by: Catherine (Katie) Buck

The basic financial advice for young adults is building an emergency fund to take care of those unexpected medical bills or car repairs and making sure you’re taking advantage of the employer match in your 401(k). However, there is a new behavioral trend towards money, a view shared mostly by younger generations, that encourages people to spend more and save less known as “soft saving”. Negative sentiment towards the higher standard of livings costs, larger debt balances, and unprecedented current events have some convinced that saving for retirement is futile and life should be enjoyed to the fullest. In this blog, I hope to encourage people to take the take control of their finances and gain some peace of mind through building an emergency fund and investing early.

Topics covered in this Blog:

- What is soft saving.

- What is an Emergency Fund.

- The Benefits of Compound Interest.

Soft Saving

Soft saving is a trend where young adults around the ages 18-25 prioritize quality of life versus grinding out an early retirement. Young adults often feel disillusioned as they face high inflation and ever-increasing costs of living while carrying generational amounts of student loan debt. In some cases, they feel as if they will never be able to save enough to fully retire. Therefore, instead of living a frugal lifestyle, they decide to live in the present and enjoy their cashflow to the fullest. Unfortunately, soft saving might be adversely impacting young investors by failing to leverage the benefits of compounding and leaving them vulnerable to incurring additional debt.

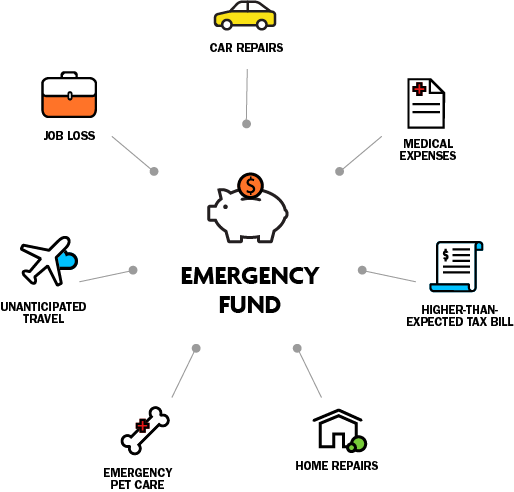

Emergency Funds

An emergency fund is 3-6 months of expenses set aside for unexpected expenses. Usually, these costs are unforeseen medical expenses, car repairs or home maintenance. This financial cushion helps avoid incurring additional debt, especially debt with higher interest rates. Having an emergency fund creates smoother budgeting, allowing for allocation towards financial goals, paying down debt or saving for a home. Emergency funds are readily accessible. Balances maintained in retirement plans like a 401(k) or IRA may be subject to withdrawal penalties. Lastly, an emergency fund can provide peace-of-mind against life’s uncertainties, greatly reducing the emotional toll of the unknown.

Compound Interest

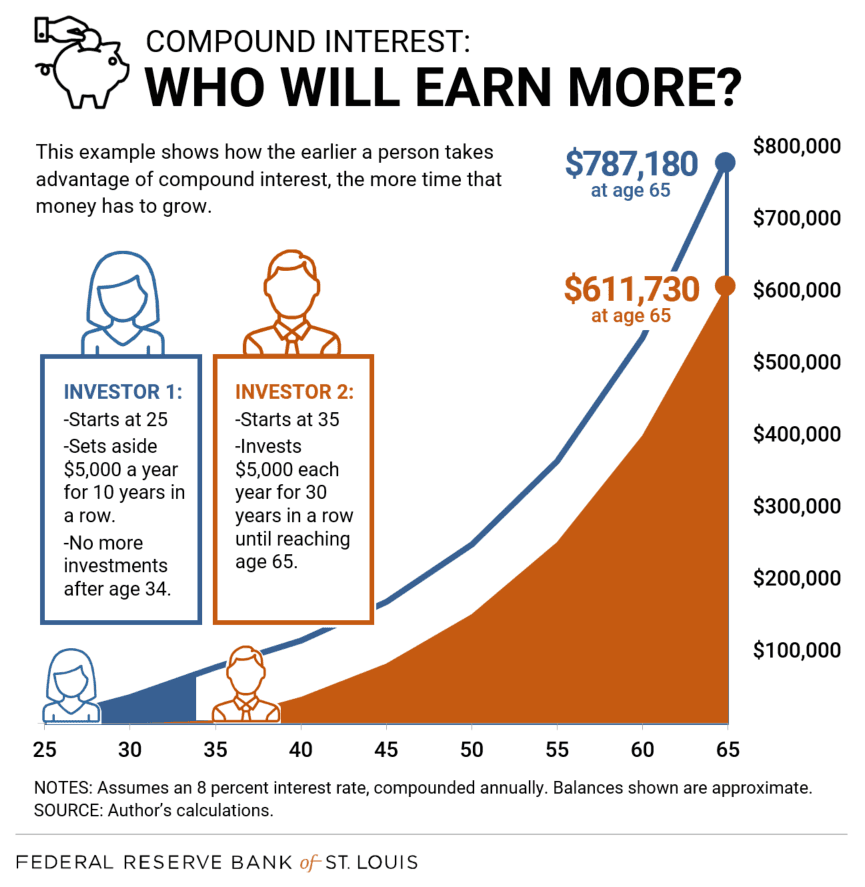

As a young adult, the power of compound interest can make even the smallest of investments appreciate exponentially long-term. Simply put, compound interest involves the reinvestment of earnings back into the investment. This continuous cycle of reinvestment contributes to the compounding effect, creating a self-reinforcing mechanism for wealth accumulation. The most important part of the equation is time, starting early and allowing compound interest to work its magic can produce returns incomparable to those who invest later in life in greater amounts. We recommend everyone take advantage of any employer retirement plan matches. For young adults, contributing a total of 10%-15% (including the employer match) is recommended. However, any contributions up to and over the employer match is beneficial if you cannot contribute up to the recommended amount. For those interested in seeing the power of compound interest relevant to their particular situation you can use this compound interest calculator provided by the S.E.C.

Conclusion

Although young adults may feel retirement is unattainable in this economy, there are some small, yet effective steps they can take to improve their financial health. Setting up an emergency fund with 3-6 months of expenses and taking advantage of employer retirement plan matches can help with their current and future standard of living. If you have questions and would like to discuss your or a loved one’s financial future, please reach out to the team at Bouchey Financial Group.

Bouchey Financial Group has offices in Saratoga Springs and Historic Downtown Troy, NY as well as Boston, MA and Jupiter, FL.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Bouchey Financial Group, Ltd. [“Bouchey Financial”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, no portion of this discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Bouchey Financial. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Neither Bouchey Financial’s investment adviser registration status, nor any amount of prior experience or success, should be construed that a certain level of results or satisfaction will be achieved if Bouchey Financial is engaged, or continues to be engaged, to provide investment advisory services. Bouchey Financial is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Bouchey Financial’s current written disclosure Brochure and Form CRS discussing our advisory services and fees is available for review upon request or at www.bouchey.com. Please Note: Bouchey Financial does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Bouchey Financial’s web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a Bouchey Financial client, please contact Bouchey Financial, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.