Reaching Record Highs

Market Overview

We started 2013 with a brief trip over the “fiscal cliff” followed by general concern over Washington bringing uncertainty to the economy and producing artificial crisis situations over the debt and budget debate. By the end of the quarter, Congress was not able to come to agreement on a master plan to change the structural issues with the federal budget but they did manage to permanently extend the Bush tax cuts for the majority of taxpayers. They were also able to increase revenue and decrease expenditures to temporarily assuage concerns over the long-term debt issue while investors ignored the ongoing debates over the debt ceiling and sequestration to drive the market rally forward.

With Washington not in the forefront of investors’ minds, the market was able to focus more on corporate profits and economic fundamentals and the end result was a very strong performance for US equities and mixed results for foreign equities.

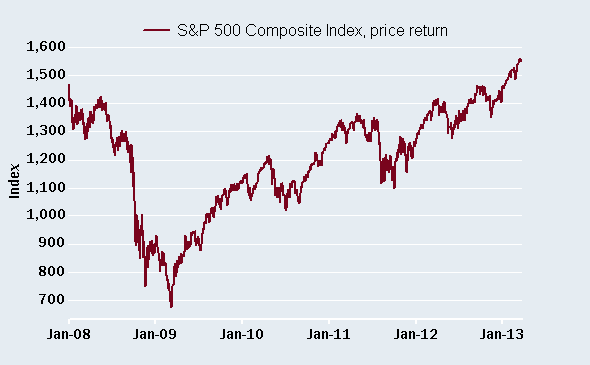

In the US, the S&P 500 index was up 10.03% to exceed its all time high reached in the fall of 2007, the Dow Jones Industrial Average was up 11.25% its strongest quarter in 15 years and the NASDAQ Composite was up 8.21%.

(Exhibit 1)

Source: Charles Schwab, FactSet, Standard & Poor’s. As of Mar. 21, 2013.

The Dow Jones All REIT index was up 10.48% for the first quarter while Gold saw a decline of 3.7%. The 10 Year US Treasury rate increased modestly by 9 basis point to 1.87% by the end of the quarter.

With International equity markets, the MSCI EAFE index was up 5.23% for the quarter, while the MSCI Emerging Markets index was down 1.57% for the quarter. The international bond markets had a very poor quarter with the J.P. Morgan Global Government Bond index down 4.18% and the J.P. Morgan Emerging Market Bond Index down 3.3% for the quarter.

Domestic Insight

From an economic perspective, the domestic data continues to show improvement in a slow but steady fashion. Consumer spending climbed in February by 0.7 percent, the most in five months and consumer sentiment (Exhibit 2) unexpectedly improved in March, both indicators showing that families at this point are not being impacted by the increase in the payroll tax or concerns over sequestration. Increases in consumer spending can be attributed to the rise in household net worth being driven by the growth in the stock market and also the rise in home valuations. With the increase in net worth, consumers are spending more and saving less. Consumer sentiment is still below its historical average which bodes well for continued positive momentum in this indicator.

(Exhibit 2)

Similarly, modest but consistent strength was also seen in the labor and housing markets. With the labor markets for the six months prior to March we saw average job growth of 196,000 jobs per month. With concerns over sequestration, the jobs number declined significantly in March with only 88,000 jobs added and an unemployment rate of 7.6%. As we’ve seen in previous month’s data, there is potential for the March number to be higher once all data is collected. The initial jobless claims showed improvement this quarter with the four week moving average declining to 343,000 as shown in Exhibit 3 below.

(Exhibit 3)

Source: BeSpoke

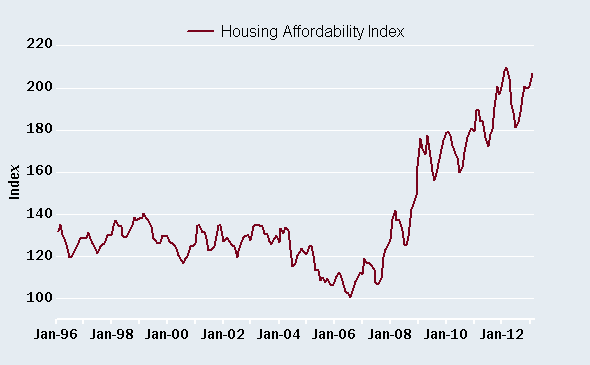

In the housing market, construction jobs moved from declining month over month over the past 4 years to strong monthly job increases this quarter. Simultaneously, with lower interest rates, reasonable prices and increasing wages, the affordability of real estate as shown in Exhibit 4 continues to improve to the strongest position in many years.

(Exhibit 4)

Source: FactSet, Nat’l Assoc. of Realtors. As of Mar. 21, 2013.

International

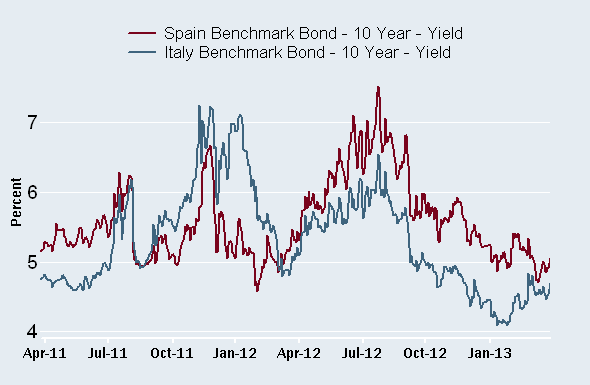

The performance of the international equity markets continues to be very mixed with countries such as Switzerland and Sweden up by 16.67% and 9.80% respectively for the quarter while Italy and Spain were down 9.77% and 5.35% respectively for the quarter. There are a number of drivers behind these numbers including the uncertainty in Italy’s election for Prime Minister and the potential for the failed administration of Silvio Berlusconi to regain control. The small nation of Cyprus requiring a bailout for its banking system and the implementation of capital controls to keep euros from flowing off the island created some volatility, but fortunately its economy is smaller than that of Vermont and it hasn’t had the same impact that a crisis would have had in a larger Euro Zone country. Finally, there is North Korea and the unpredictable statements and actions of its young, new leader Kim Jong-un to remind all of us that we live in an uncertain global economy.

Even with this mixed performance and the geo-political issues highlighted above, the valuation of many developed and emerging market equity indices present good long-term investments at very reasonable valuations. Both developed and emerging market countries are trading below their historical averages, creating good buying opportunities. Also, as is shown in Exhibit 5 below, the risk quotient in Europe has increased but based on the 10 year bond yield in Italy and Spain that increase is well below the fears and concerns of the prior years.

(Exhibit 5)

Source: Charles Schwab, FactSet, iBoxx. As of Mar. 27, 2013

Fixed Income

As we started 2013 there were expectations that the “great rotation” out of bonds and into stocks would begin as investors, concerned that interest rates could be rising, would see their bond portfolios decline while equity values increased. After the completion of the 1st quarter it is reasonable to say that this process has yet to begin. The rotation that IS happening is out of cash, $43 billion year-to-date, in additional to the $151 billion in 2012, and into real estate, equities and bonds. This type of investment behavior is exactly what the Federal Reserve was hoping to achieve by keeping interest rates low and through its quantitative easing initiatives.

High yield bonds were one category in particular that experienced strong performance this quarter, buoyed by the strong economic data, positive stock market performance, and investors’ continued search for yield.

Weakness was seen in long-term bonds which declined by 1.72% as the market began anticipating higher interest rates and with emerging market bonds due to weakness in the commodity markets and weaker than anticipated economic reports for several emerging market economies.

Outlook for the Remainder of 2013

After such a strong quarter the obvious question becomes, where do we go from here? The answer points to more positive quarters but there is still enough economic uncertainty that there is the potential for a market pull back at some point.

There are a number of factors that support the market momentum continuing and the best way to illustrate this possibility is to compare current metrics to those from the previous market peak in October 2007.

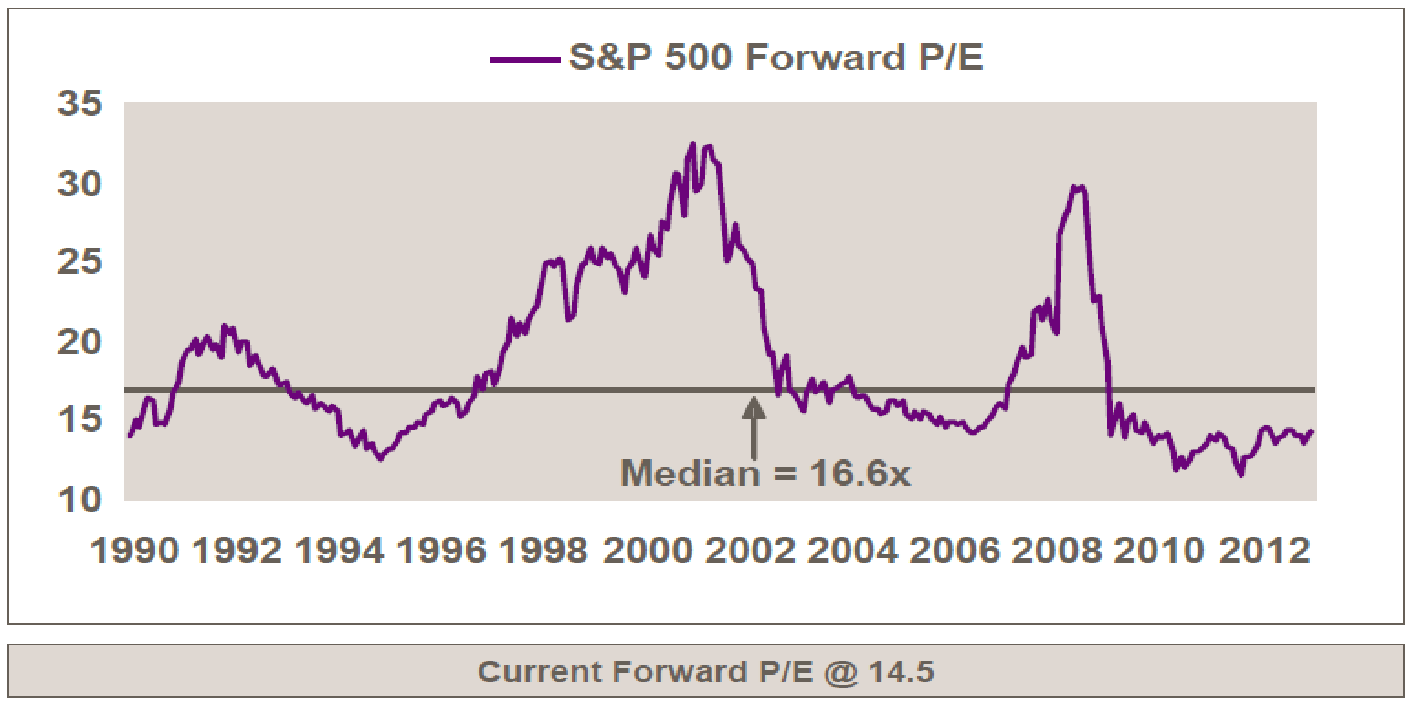

One of the most important metrics to consider is the current valuations on stocks which are considerably lower than what they were in 2007 and even lower than historical average. The best metric to show this is the price to earnings (PE) ratio of the S&P 500 index. In 2007, the S&P 500’s PE ratio was in the 20s. As of the quarter’s close, the forward and trailing PE ratios are 14.5 and 15.5 times, respectively, still below the historical average shown in Exhibit 6 below. It is also the case that dividends are substantially higher than in 2007 with more than 400 companies currently paying dividends, the highest since 1998 and the current average dividend yield of 2.45% is well above the 1.89% rate from the fourth quarter of 2007. The other item to consider is the return potential of other investment options versus the stock market. The 10-year Treasury yield is currently below 2%, compared to its rate of around 4.5% in 2007, making investing in stocks much more attractive at this point.

(Exhibit 6)

Source: Charles Schwab

In an average year, there will be five corrections in the market each with a decline of 5% or greater. Since November of last year, we have not experienced a correction of this magnitude so statistically speaking we could see a pullback at some point. It is also the case that along with reasonably strong economic data this quarter there has been some weakness shown more recently with the Institute for Supply Management (ISM) index dropping to 54.4 in March from 56 and the March labor report. Readings above 50 indicate expansion but this data point was below most economist expectations.

With that said, we are still optimistic that a well-diversified portfolio and a long-term outlook on the markets is the best approach in this environment. Although we saw emerging markets underperform in the first quarter, we are confident there is room to grow in this asset class. With historically low prices, GDP growth in the high single digits (compared to 2% in the US) and an overall GDP that makes up 51% of the world’s economy, it’s important to have exposure to these markets.