Wealth Management Near Walpole MA | Norfolk County Fiduciary RIA

Walpole carries a median household income of $159,720 and a poverty rate of just 2.8%, per U.S. Census Bureau data — a profile built on peak-earning professionals and business owners with real planning complexity. For households at this level, the type of advisory relationship matters as much as the quality of the advisor. Bouchey Financial Group is a fiduciary Registered Investment Advisor serving Walpole and Norfolk County from its Medfield office.

The team manages over $1.6 billion in assets for clients in 34 states, with 9 CERTIFIED FINANCIAL PLANNER™ professionals, 3 CPAs, 1 IRS Enrolled Agent, and a Certified Private Wealth Advisor® — all fee-only, no commissions.

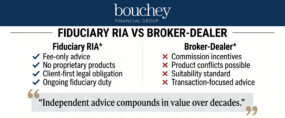

What It Means to Work With a Fiduciary RIA

A Registered Investment Advisor is a firm registered with the SEC and legally held to a fiduciary standard — requiring the advisor to act in the client's best interest at all times, with both a duty of care and a duty of loyalty. This distinguishes RIAs from broker-dealers, whose recommendations need only meet a suitability or "best interest" standard under Regulation Best Interest — a lower threshold that still permits compensation-driven product recommendations.

| Fiduciary RIA | Broker-Dealer | |

| Legal standard | Fiduciary duty (duty of care + loyalty) | Regulation Best Interest / Suitability |

| Compensation | Fee-only (client-paid) | Commissions + fees |

| Product conflicts | None — no proprietary products | Possible — compensation tied to sales |

| Ongoing obligation | Continuous | At time of recommendation only |

Why Independence Compounds in Value Over Time

An independent RIA has no affiliated products to sell, no internal revenue targets tied to specific investments, and no institutional pressure to steer clients toward managed accounts with embedded fees. According to the SEC's guidance on adviser standards of conduct, the duty of loyalty specifically requires an adviser to eliminate or disclose conflicts — not simply to manage them in good faith.

Over a 20- to 30-year advisory relationship, the compounding effect of unbiased recommendations — consistently directed toward the client's actual best interest — is one of the most underappreciated drivers of long-term wealth outcomes.

Retirement Planning in a High-Income Norfolk County Household

The Boston College Center for Retirement Research tracks the National Retirement Risk Index, which measures the share of working households at risk of being unable to maintain their pre-retirement standard of living. Despite recent improvements driven largely by rising home values, the Index shows that a significant portion of American households — even those with high current income — remain exposed to retirement shortfalls due to inadequate savings, poor distribution sequencing, or underestimated longevity.

For Walpole-area professionals with household incomes above $159,000, the risk profile is different from the national average but not absent. The planning gaps for high-income households typically involve tax exposure, distribution timing, and the failure to integrate investment and tax strategy — rather than savings levels alone.

Coordinating Multiple Retirement Income Sources

A typical Walpole-area retirement plan involves Social Security, one or more 401(k) or IRA accounts, taxable investment accounts, potential pension income, and Massachusetts real estate equity. Drawing these sources down in the right sequence — taxable accounts first, then tax-deferred, then Roth — can meaningfully reduce lifetime tax liability and extend portfolio longevity.

Bouchey Financial Group's investment management approach integrates distribution strategy directly into each client's financial plan, coordinated with the firm's in-house CPAs who model the tax implications of each withdrawal decision year by year.

Tax-Efficient Investing for Walpole Professionals

Tax efficiency is one of the highest-leverage dimensions of wealth management — and one of the least visible. The difference between a tax-aware and tax-indifferent investment strategy compounds significantly over time through three primary levers: asset location, tax-loss harvesting, and capital gains timing.

According to the IRS Topic 409 on capital gains and losses, capital losses can be used to offset capital gains dollar-for-dollar — and up to $3,000 of excess losses per year can offset ordinary income. Tax-loss harvesting systematically realizes losses in underperforming positions to generate this offset, while maintaining portfolio exposure through similar (not substantially identical) replacement holdings.

The Massachusetts Tax Layer

Massachusetts imposes a 5% flat income tax rate with an additional 4% surtax on taxable income above $1,107,750 in 2026. For Walpole households realizing large capital gains through equity compensation, business sales, or investment liquidations, managing the timing and character of those gains against both federal and state thresholds requires year-round coordination — not a year-end adjustment.

Bouchey Financial Group's in-house CPAs integrate this analysis into each client's plan, ensuring that investment decisions and tax decisions are made together rather than in sequence.

Estate Planning and Wealth Preservation in Norfolk County

Massachusetts maintains a $2 million estate tax exemption — significantly lower than the federal threshold — with graduated rates up to 16%, per Mass.gov's official estate tax guidance. For Walpole households with real estate, retirement accounts, and investment assets that together approach or exceed that threshold, estate planning is a practical necessity rather than a deferred consideration.

Bouchey Financial Group coordinates with clients' estate attorneys to align trust structures, beneficiary designations, and gifting strategies with the broader financial plan. The firm's Why Bouchey Financial Group page outlines this multi-discipline coordination in detail.

Concentrated Stock and Equity Compensation

For Walpole-area professionals who have accumulated equity compensation — restricted stock units, stock options, or employee stock purchase plans — managing concentration risk requires a structured approach to vesting, tax-lot selection, and diversification timing. Concentrated positions that have appreciated significantly carry embedded capital gains that must be managed carefully to avoid triggering large tax events in a single year.

Bouchey Financial Group's advisors build liquidation strategies around each client's full income picture, Massachusetts surtax exposure, and long-term portfolio objectives. The Individuals & Families page details the firm's approach to portfolio customization for complex household situations.

Women, Wealth, and the Fiduciary Relationship

Norfolk County has a high concentration of dual-income professional households and women who manage significant financial assets independently — through career income, business ownership, or transitions such as divorce or inheritance. Bouchey Financial Group's Women and Wealth initiative, led by Harmony Wagner, CFP®, CPWA®, Samantha Masey, CFP®, and Catherine Buck, CFP®, addresses the specific planning dimensions that matter most to women navigating long-term financial independence.

Women statistically outlive men by several years, making longevity planning — portfolio sustainability, Social Security timing, and long-term care coordination — especially relevant in the context of a fiduciary advisory relationship.

Starting the Right Advisory Relationship

Walpole-area households with meaningful accumulated assets deserve an advisory relationship grounded in legal obligation — not aspiration. Bouchey Financial Group's fiduciary RIA structure, in-house CPA and tax expertise, and fee-only compensation model put the firm on the same side of the table as its clients from the first conversation.

To schedule a complimentary consultation at the Medfield office, contact the team directly.

Frequently Asked Questions

What does "fiduciary" mean in the context of financial advice?

A fiduciary is legally required to act in a client's best interest at all times — a standard that encompasses both a duty of care (recommendations must reflect the client's actual situation and goals) and a duty of loyalty (the adviser's interests cannot take precedence over the client's). This is a higher legal standard than the suitability requirement applied to broker-dealers, which permits recommendations influenced by compensation as long as they are broadly appropriate.

What is the difference between an RIA and a broker?

A Registered Investment Advisor is a firm registered with the SEC and held to fiduciary duty. A broker-dealer is registered with FINRA and required only to meet a suitability or best-interest standard under Regulation Best Interest. The practical difference is compensation structure: RIAs are typically paid by clients, while brokers are often compensated through commissions on products sold — creating incentives that can influence recommendations.

What is tax-loss harvesting, and how does it work?

Tax-loss harvesting is the practice of selling a security that has declined in value to realize a capital loss, which can offset capital gains realized elsewhere in the portfolio. The position is replaced with a similar (but not substantially identical) holding to maintain market exposure. The IRS allows capital losses to offset capital gains dollar-for-dollar, with up to $3,000 of excess losses per year deductible against ordinary income. For high-income Massachusetts households, this strategy is most valuable when coordinated against both federal and state tax exposure.

How often should a portfolio be rebalanced?

There is no universal rule, but most advisors rebalance when asset class weightings drift significantly from target allocations — typically a 5% threshold. In tax-sensitive accounts, rebalancing decisions also account for capital gains implications, directing trades to tax-deferred accounts where possible to avoid triggering taxable events. Annual reviews provide a baseline, with additional rebalancing triggered by significant market movements or changes in a client's income or time horizon.

When should someone near Walpole consider hiring a wealth manager?

The most common triggers are approaching retirement with multiple income sources to coordinate, accumulating investable assets above $500,000, receiving a liquidity event from a business or inheritance, or reaching a level of income and tax complexity — equity compensation, Massachusetts surtax exposure, real estate holdings — that a basic advisor relationship doesn't address. Bouchey Financial Group's $500,000 minimum reflects the depth of the integrated planning work the firm provides.

How do fiduciary advisors get paid?

Fee-only fiduciary advisors are paid directly by clients — typically through a percentage of assets under management, a flat retainer, or hourly fees. No commissions, no product markups, and no third-party compensation of any kind. The AUM model means the advisor's revenue increases only when the client's portfolio grows, directly aligning both parties' interests over time.

Should retirees rebalance portfolios differently than pre-retirees?

Yes — the approach to rebalancing shifts meaningfully in retirement because the portfolio is now a distribution vehicle rather than a pure accumulation vehicle. Retirees typically maintain a liquidity reserve to cover one to three years of spending, reducing the need to sell equities in poor market years. Rebalancing is also coordinated with the distribution sequence — drawing from overweighted asset classes first to naturally rebalance while meeting income needs, rather than selling purely for allocation reasons.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Bouchey Financial Group, Ltd. [“Bouchey Financial”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, no portion of this discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Bouchey Financial. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Neither Bouchey Financial’s investment adviser registration status, nor any amount of prior experience or success, should be construed that a certain level of results or satisfaction will be achieved if Bouchey Financial is engaged, or continues to be engaged, to provide investment advisory services. Bouchey Financial is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Bouchey Financial’s current written disclosure Brochure and Form CRS discussing our advisory services and fees is available for review upon request or at www.bouchey.com. Please Note: Bouchey Financial does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Bouchey Financial’s web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a Bouchey Financial client, please contact Bouchey Financial, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.