Wealth Management Near Millis MA | Serving Greater Medfield Area

Millis is one of Norfolk County's most financially stable communities, with a median household income of $155,996, a homeownership rate of 75.8%, and a median age of 46.4, per U.S. Census Bureau data. That demographic profile — heavily weighted toward peak-earning and pre-retirement households — creates a specific planning need: protecting and coordinating wealth that's already been built. Bouchey Financial Group serves the Greater Medfield area from its office at 50 North Street in Medfield, operating as a fee-only, fiduciary RIA.

The firm manages over $1.6 billion in assets for clients in 34 states, with 9 CERTIFIED FINANCIAL PLANNER™ professionals, 3 CPAs, 1 IRS Enrolled Agent, and a Certified Private Wealth Advisor®.

What Wealth Management Actually Includes

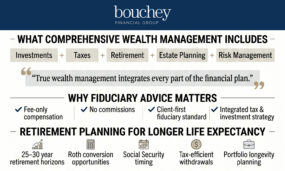

"Wealth management" means different things depending on the firm. In a genuine comprehensive relationship, it integrates several disciplines that most households need to manage simultaneously:

- Investment management — portfolio construction, rebalancing, asset location, and ongoing monitoring

- Tax planning — Roth conversions, capital gains timing, loss harvesting, and distribution sequencing

- Retirement income planning — withdrawal strategy, Social Security timing, and RMD coordination

- Estate coordination — trust structures, beneficiary review, and titling aligned with the estate plan

- Risk management — insurance review and asset protection analysis

At Bouchey Financial Group, these services are integrated under one roof — not outsourced across separate specialists who don't communicate with each other.

How to Evaluate a Financial Advisor in the Greater Medfield Area

Before entering any advisory relationship, households should verify credentials and registration. FINRA's BrokerCheck is a free public tool that shows an advisor's employment history, licenses, exam qualifications, and any disciplinary history. For RIAs specifically, the SEC's Investment Adviser Public Disclosure database provides the firm's Form ADV — the disclosure document that details compensation structure, conflicts of interest, and services offered. Both tools take minutes to use and should be standard practice before signing any advisory agreement.

The key questions to ask before committing to an advisor relationship are straightforward: Are you a fiduciary at all times? Are you fee-only? Do you have CPAs on staff? What is your minimum? Bouchey Financial Group answers yes to the first three.

Credentials That Matter

Not all financial designations carry the same weight. The CFP® designation requires 6,000 hours of professional experience, a comprehensive exam, ongoing continuing education, and adherence to a fiduciary code of ethics administered by the CFP Board.

The CPA credential requires state licensure and is the recognized standard for tax expertise. Bouchey Financial Group's team holds both, with CPAs and CFP® professionals working together on each client's plan.

Retirement Income Planning for Greater Medfield Households

With a median age of 46.4, a significant share of Millis households are within 15 to 20 years of retirement — close enough that planning decisions made today have direct consequences on retirement outcomes. The Stanford Center on Longevity notes that with people increasingly living into their 80s and 90s, funding a 30-year retirement on a 40-year career has become one of the defining financial challenges of our era, requiring more deliberate savings, distribution strategy, and longevity planning than prior generations faced.

For Greater Medfield professionals, that challenge is most acute around distribution sequencing — the order in which retirement accounts are drawn down, when Social Security is claimed, and how income is structured to minimize lifetime tax liability across potentially three decades.

Roth Conversions and the Window Before RMDs

The period between retirement and when required minimum distributions begin at age 73 represents a valuable tax planning window. During this time, income is often at its lowest, making Roth conversions — moving assets from traditional IRAs into Roth accounts — more efficient than at any other point in the financial life cycle.

Bouchey Financial Group's investment management approach integrates Roth conversion modeling directly into each client's financial plan, coordinated with in-house CPAs who evaluate the Massachusetts and federal tax implications year by year.

Tax-Efficient Investing for Norfolk County Households

Massachusetts taxes most retirement income at 5%, with an additional 4% surtax on taxable income above $1,107,750 in 2026, per the Massachusetts Department of Revenue. Notably, Massachusetts does exempt Social Security benefits from state income tax, and residents 65 and older may qualify for the Senior Circuit Breaker tax credit — worth up to $2,820 for tax year 2025, per the Massachusetts DOR. For households with multiple income sources, understanding which are taxable at the state level and which are exempt changes the sequencing calculus meaningfully.

Asset location — placing tax-inefficient investments such as bonds in tax-deferred retirement accounts, and tax-efficient investments such as index funds in taxable accounts — is one of the highest-leverage, lowest-visibility strategies available to high-income households. Bouchey Financial Group's in-house CPA team builds this into every client's portfolio construction from day one.

Estate Planning Coordination for Greater Medfield Families

For households in Millis and the surrounding area with combined assets — real estate, retirement accounts, taxable investments, and potential business interests — estate planning is a coordination problem as much as a legal one. Massachusetts's $2 million estate tax exemption, per Mass.gov's estate tax guidance, sits far below the federal threshold, meaning families with meaningful accumulated assets face state-level exposure even when they owe nothing federally.

Bouchey Financial Group coordinates with clients' estate attorneys on trust structures, beneficiary designations, and account titling to ensure that the investment plan and estate plan work in the same direction. The Why Bouchey Financial Group page outlines the firm's integrated advisory model in detail.

Legacy Planning and the Next Generation

For Greater Medfield families with a homeownership rate of 75.8% and decades of professional income behind them, the conversation about intergenerational wealth transfer is often more relevant than they expect. Gifting strategies, trust structures, and beneficiary designation reviews all affect how efficiently assets pass to the next generation — and how much of that transfer is subject to Massachusetts estate tax.

Harmony Wagner, CFP®, CPWA®, Samantha Masey, CFP®, and Catherine Buck, CFP® lead Bouchey Financial Group's Women and Wealth initiative, with particular focus on women navigating wealth transitions, inheritance, and long-term financial planning for their families.

Local Planning, Experienced Team

Greater Medfield area households deserve an advisory team that understands Massachusetts tax law, is physically accessible, and brings genuine credential depth to every dimension of the financial plan. Bouchey Financial Group's Medfield office puts a fee-only, fiduciary team within reach — no commissions, no conflicts, and no need to coordinate between separate firms for investment and tax strategy.

To schedule a complimentary consultation, contact the team at the Medfield office.

Frequently Asked Questions

What's included in comprehensive wealth management?

Comprehensive wealth management integrates investment management, tax planning, retirement income strategy, estate coordination, and risk management under one advisory relationship. The value comes from the integration — tax decisions inform investment decisions, and distribution strategy shapes the estate plan — rather than any single service in isolation.

What is a fiduciary financial advisor?

A fiduciary is legally required to act in your best interest at all times, with a duty of care and a duty of loyalty that cannot be waived. This is a higher standard than the suitability requirement applied to broker-dealers, which permits recommendations that benefit the advisor financially as long as they are broadly appropriate for the client.

How often should I review my financial plan?

Formally at least once per year, and after any significant life event — a job change, inheritance, health event, or major market shift. Annual reviews catch drift in asset allocation, outdated beneficiary designations, and tax planning opportunities that have opened or closed since the last review.

What investment mistakes do retirees commonly make?

The most consequential are drawing down accounts in the wrong order (triggering unnecessary taxes), claiming Social Security too early (permanently reducing monthly benefits), and holding too little equity exposure for a 25- to 30-year retirement horizon. Each mistake is avoidable with proper planning, but difficult to reverse once made.

How do wealthy families minimize taxes in retirement?

The most impactful strategies are Roth conversions during low-income years, drawing taxable accounts before tax-deferred ones, directing rebalancing through retirement accounts to avoid capital gains, and using qualified charitable distributions from IRAs after age 70½. Each strategy's value depends on the full income picture, which is why having CPAs integrated into the advisory relationship matters.

Should I choose a local financial advisor?

Local advisors are more likely to understand Massachusetts-specific tax considerations — the 5% income tax, the 4% surtax, the $2 million estate tax threshold — that national platforms applying standardized models routinely miss. Proximity also supports the kind of ongoing, relationship-driven planning that adjusts with your circumstances over time.

What is estate planning coordination, and why does it matter?

Estate planning coordination means ensuring that your investment strategy, account titling, beneficiary designations, and trust structures all work together toward the same outcome. Without coordination, it's common for a carefully drafted will to be effectively overridden by an outdated beneficiary designation on a retirement account — directing assets to the wrong person regardless of what the legal documents say.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Bouchey Financial Group, Ltd. [“Bouchey Financial”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, no portion of this discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Bouchey Financial. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Neither Bouchey Financial’s investment adviser registration status, nor any amount of prior experience or success, should be construed that a certain level of results or satisfaction will be achieved if Bouchey Financial is engaged, or continues to be engaged, to provide investment advisory services. Bouchey Financial is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Bouchey Financial’s current written disclosure Brochure and Form CRS discussing our advisory services and fees is available for review upon request or at www.bouchey.com. Please Note: Bouchey Financial does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Bouchey Financial’s web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a Bouchey Financial client, please contact Bouchey Financial, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.