Wealth Management Near Medfield MA | Serving Norfolk County

Norfolk County carries a median household income of $139,076 — more than 1.5 times the national median — and a poverty rate of just 6.3%, according to Census Reporter. For the executives, physicians, and business owners who make up much of Medfield's professional base, accumulated wealth demands a coordinated plan. Bouchey Financial Group serves Norfolk County from its Medfield office at 50 North Street as a fee-only, fiduciary RIA.

The firm manages over $1.6 billion in assets for clients in 34 states, with a team of 9 CERTIFIED FINANCIAL PLANNER™ professionals, 3 CPAs, 1 IRS Enrolled Agent, and a Certified Private Wealth Advisor® — compensated only by clients, with no commissions and no proprietary products.

Why Norfolk County Households Seek Fiduciary Guidance.

The term "fiduciary" has a specific legal meaning. As defined by SEC guidance on investment adviser standards, a registered investment adviser owes clients both a duty of care — acting on their best interest — and a duty of loyalty — placing the client's interests above the firm's own. Neither obligation can be waived.

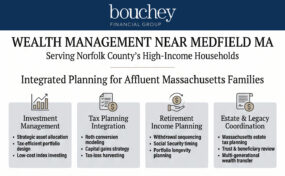

For Norfolk County clients, that translates into a planning relationship encompassing investment management, retirement income strategy, tax planning, and estate coordination — fully integrated, not siloed.

Massachusetts Tax Planning for High-Income Households

Massachusetts imposes a 5% flat income tax rate, with an additional 4% surtax on taxable income exceeding $1,107,750 in 2026, per the Massachusetts Department of Revenue. For high-earning Medfield-area professionals, this creates meaningful state tax exposure that interacts directly with investment decisions, retirement distributions, and business income.

Bouchey Financial Group's team includes 3 CPAs and 1 IRS Enrolled Agent who integrate tax strategy directly into the wealth management relationship. Roth conversion modeling, capital gains timing, and tax-loss harvesting are evaluated annually as part of each client's financial plan, not as standalone year-end adjustments.

The Massachusetts Estate Tax: A Critical Planning Threshold

Massachusetts maintains one of the lowest estate tax exemptions in the country. According to Mass.gov's official estate tax guidance, estates exceeding $2 million are subject to state estate tax at graduated rates ranging from 0.8% to 16%. The federal exemption is $15 million per person — meaning many Massachusetts estates that owe nothing federally still carry significant state exposure.

For Norfolk County households with real estate, investment accounts, retirement assets, and business interests that together approach or exceed $2 million, estate planning is not optional. It is one of the most high-value activities a wealth advisor can facilitate.

Retirement Income Planning for Boston-Area Professionals

For Medfield-area households in peak earning years, retirement planning involves more than accumulation. The transition from a high-income career to a sustainable distribution strategy requires sequencing decisions that affect decades of tax liability and portfolio longevity.

The IRS sets the 2026 401(k) contribution limit at $24,500, with an $8,000 catch-up for those 50 and older. For Massachusetts professionals in the top income brackets, maximizing pre-tax contributions reduces both federal and state taxable income — a compounding benefit in a high-tax environment.

Roth Conversions and Withdrawal Sequencing

Converting traditional IRA assets to Roth during lower-income years — before Social Security, before required minimum distributions, and before other income sources activate — can materially reduce lifetime tax liability. This strategy requires careful modeling against each client's expected income trajectory, bracket thresholds, and Medicare premium exposure.

Bouchey Financial Group's investment management approach integrates these decisions across the full financial plan, ensuring that portfolio construction and distribution strategy move together rather than independently.

Investment Management for Norfolk County Clients

Portfolio construction for affluent households goes beyond diversification. It involves asset location — placing tax-efficient holdings in taxable accounts and tax-inefficient holdings in retirement accounts — ongoing rebalancing, and a disciplined framework for managing market volatility without abandoning long-term strategy.

According to the FINRA Foundation's National Financial Capability Study, even among higher-income households, a meaningful share report difficulty with investment confidence and retirement preparedness — a gap that professional advisory relationships consistently close. Bouchey Financial Group uses index funds for the majority of holdings, keeping expense ratios low and minimizing tax drag from unnecessary turnover.

Risk Management and Portfolio Longevity

Market sequence risk — the impact of a poor early return on a retirement portfolio — is one of the most underappreciated planning variables. A portfolio that loses value in the first years of retirement, while distributions are still being taken, recovers more slowly than the same portfolio experiencing the same loss during accumulation.

Managing this risk requires building a distribution strategy around expected spending needs, Social Security timing, and reserve liquidity — not simply a target asset allocation. The Why Bouchey Financial Group page outlines the firm's full investment philosophy for prospective clients.

Women and Wealth in Norfolk County

Norfolk County has an above-average concentration of dual-income professional households, and a growing share of women who manage significant personal wealth independently — whether through career earnings, business ownership, or life transitions such as divorce or inheritance. The Women and Wealth initiative at Bouchey Financial Group addresses these planning needs directly, led by Harmony Wagner, CFP®, CPWA®, Samantha Masey, CFP®, and Catherine Buck, CFP®.

Women in the Greater Boston area hold meaningful financial assets and face distinct planning considerations — including longer life expectancy, career interruptions, and a higher likelihood of managing wealth independently later in life. The firm's Women & Wealth programming reflects that reality.

A Medfield-Based Team for Norfolk County Clients

Choosing a local advisor matters when financial decisions are tied to regional tax law, estate regulations, and the economic realities of living in one of Massachusetts's most affluent counties. Bouchey Financial Group's Medfield office puts a fully credentialed, fiduciary advisory team within reach of Norfolk County residents — without requiring a trip into Boston.

To schedule a complimentary consultation and explore whether Bouchey Financial Group is the right fit, contact the team at the Medfield office directly.

Frequently Asked Questions

What is the difference between wealth management and financial planning?

Financial planning is a process — typically a one-time or periodic engagement that produces a written plan covering goals, cash flow, and projections. Wealth management is an ongoing relationship that integrates financial planning with investment management, tax strategy, estate coordination, and risk management. For high-net-worth households, the value is in the ongoing integration across all those disciplines, not any single plan or recommendation.

What is the Massachusetts millionaire's tax, and who does it affect?

Massachusetts imposes a 4% surtax on taxable income above $1,107,750 in 2026 — adjusted annually for inflation from the original $1 million threshold set in 2023 — on top of the state's standard 5% rate. For Norfolk County professionals realizing a large capital gain through a business sale, stock options, or investment liquidation, the surtax can apply in a single year even when ordinary income typically falls below that threshold.

How often should a financial plan be reviewed?

A formal plan review should occur at least annually, with additional reviews triggered by significant life events: a job change, inheritance, business exit, or major market shift. Many households set a plan in place and don't revisit it for years, allowing asset allocations to drift and tax opportunities to pass unrealized. Bouchey Financial Group's advisory model includes regular reviews as a standard part of the client relationship.

What makes a local advisor preferable to a national wealth management platform?

Local advisors with regional expertise understand state-specific tax rules — including Massachusetts's estate tax, income surtax, and pension exclusions — in a way that national platforms applying standardized models typically do not. Personalized advisory relationships also allow advisors to respond to life events and planning opportunities in real time, rather than through automated portfolio adjustments.

When should someone hire a wealth manager?

The most common decision points are: approaching retirement and needing a distribution strategy; receiving a significant inheritance or business liquidity event; accumulating investable assets above $500,000; or reaching a level of income complexity — multiple accounts, equity compensation, real estate — that exceeds what a basic advisor relationship addresses. Bouchey Financial Group works with clients at or above the $500,000 investable asset threshold.

How do high-income households minimize taxes on investment gains?

The primary strategies include: holding appreciated assets for more than one year to qualify for long-term capital gains treatment; harvesting capital losses to offset gains; directing rebalancing through tax-deferred accounts to avoid triggering taxable events; using qualified charitable distributions from IRAs after age 70½; and structuring gifting through appreciated securities rather than cash. Each strategy's applicability depends on the household's full income picture, which is why in-house CPA expertise matters.

What role does a Certified Private Wealth Advisor® play in a client relationship?

The CPWA® designation, issued by the Investments & Wealth Institute, is an advanced credential covering high-net-worth planning areas including tax minimization, concentrated position management, estate strategies, and alternative investments. It is designed specifically for advisors working with affluent clients whose planning needs exceed standard financial planning scope. At Bouchey Financial Group, Harmony Wagner, CFP®, CPWA®, holds this designation alongside her CFP® certification, bringing specialized expertise to complex client situations.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Bouchey Financial Group, Ltd. [“Bouchey Financial”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, no portion of this discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Bouchey Financial. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Neither Bouchey Financial’s investment adviser registration status, nor any amount of prior experience or success, should be construed that a certain level of results or satisfaction will be achieved if Bouchey Financial is engaged, or continues to be engaged, to provide investment advisory services. Bouchey Financial is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Bouchey Financial’s current written disclosure Brochure and Form CRS discussing our advisory services and fees is available for review upon request or at www.bouchey.com. Please Note: Bouchey Financial does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Bouchey Financial’s web site or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Please Remember: If you are a Bouchey Financial client, please contact Bouchey Financial, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.